For many years, Greece has been regarded as one of the most attractive Golden Visa markets in Europe thanks to:

- A relatively competitive investment threshold

- European residency rights

- Schengen mobility

- And the opportunity to own real estate in a fast-growing tourism market

However, the market is now changing quite significantly.

If the period between 2017 and 2024 was defined by the boom of Airbnb-style investments and short-term rental speculation in Athens, then since late 2024 the market has started entering a very different phase: A phase where operational performance and long-term rental fundamentals matter far more than tourism-driven speculation.

This transition was highlighted in a recent IMI Daily analysis examining rental yields across Greece’s Golden Visa property market.

Athens continues to lead Greece in rental yields

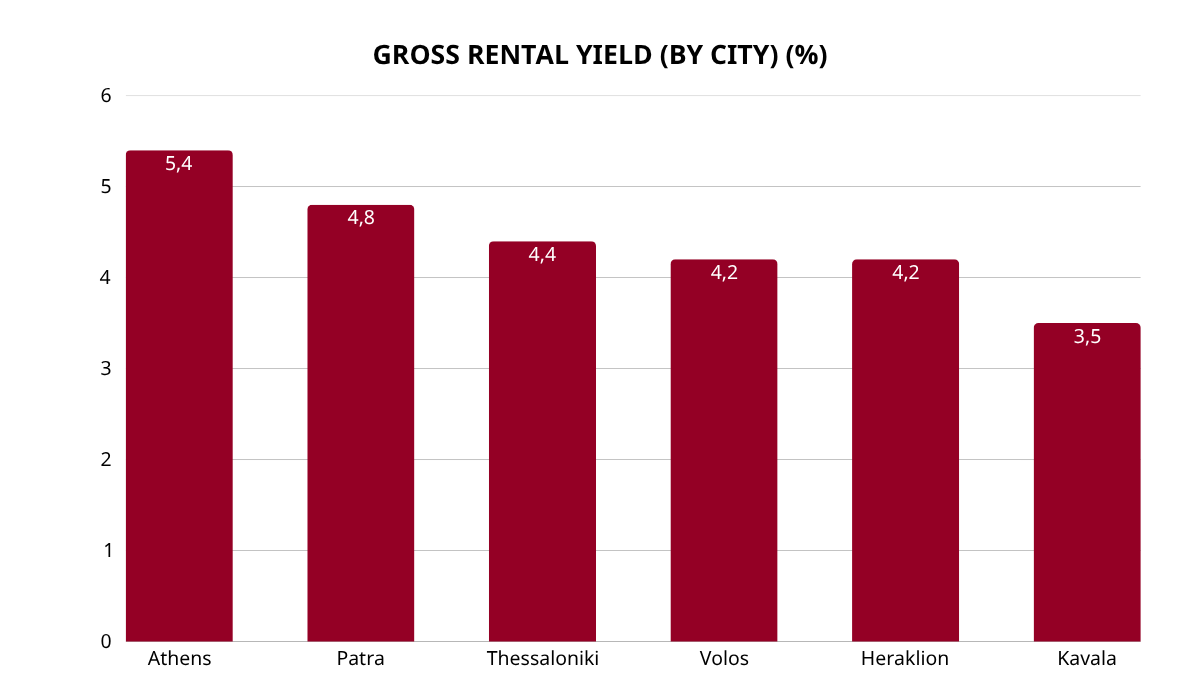

According to Global Property Guide’s November 2025 residential rental yield survey cited by IMI Daily, Athens currently delivers the highest residential rental yields among Greece’s major cities.

The report shows:

- Athens averaging approximately 5.4% gross rental yield

- Patra at 4.8%

- Thessaloniki at 4.4%

- Volos and Heraklion at around 4.2%

- Kavala at approximately 3.5%

These figures represent gross rental yields, meaning before:

- Taxes

- Management fees

- ENFIA property tax

- Maintenance costs

- And vacancy periods

According to Global Property Guide’s methodology, net yields in Greece are typically 1.5–2 percentage points lower after operational expenses.

Even after adjustments, however, Athens remains relatively competitive compared to many Western European property markets.

This reflects an important reality: Property prices in Athens still remain below many European capitals, while rental demand continues to strengthen.

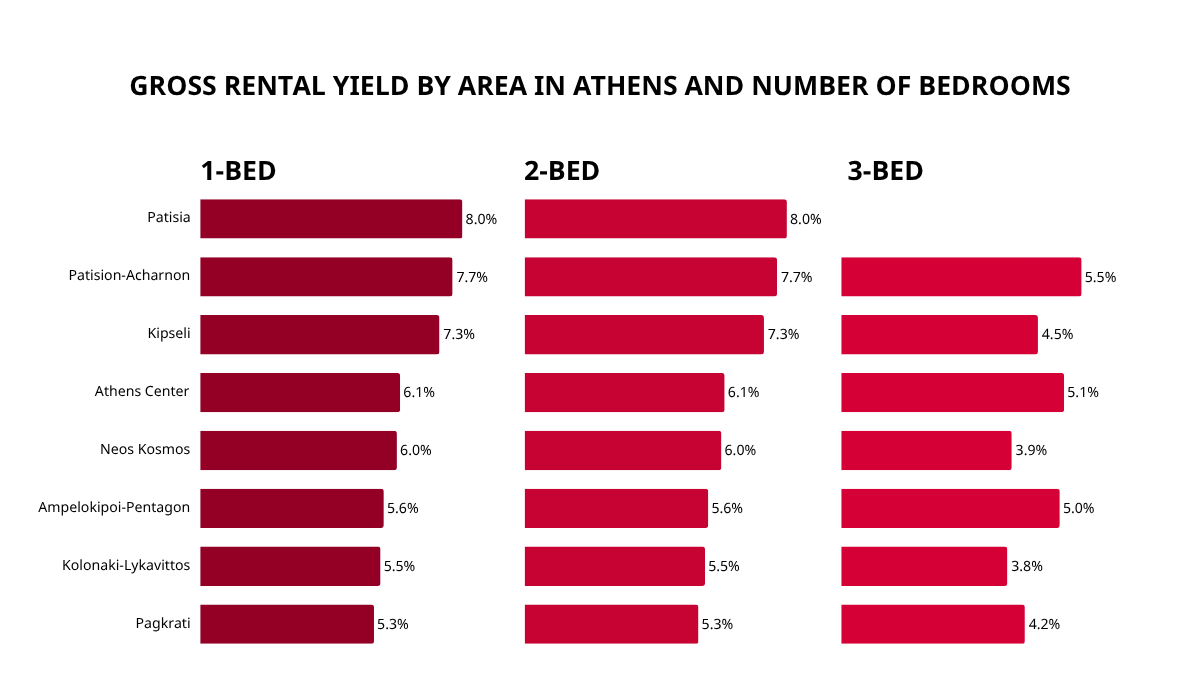

Neighborhood differences inside Athens are even larger than differences between cities

One of the most striking findings in the report is: Yield differences within Athens are greater than the differences between entire Greek cities.

For example:

- One-bedroom apartments in Patisia currently generate around 8% gross yield

- Kipseli delivers approximately 7.3%

- Central Athens averages around 6%

Meanwhile:

- A three-bedroom apartment in Kolonaki–Lykavittos — one of Athens’ most prestigious districts — delivers only around 3.8%

That figure is close to the average yield across the entire city of Kavala.

This reflects a broader market reality: Investment performance today is increasingly driven by operational demand rather than purely by prestige or luxury positioning.

Smaller apartments in middle-income urban neighborhoods are outperforming larger luxury units because they offer:

- Lower acquisition costs

- Higher occupancy rates

- Broader tenant demand

- And stronger alignment with today’s short- and medium-term living patterns

By contrast, luxury properties have seen prices rise much faster than rents, compressing their yields significantly.

Thessaloniki shows the same pattern

The same trend is visible in Thessaloniki.

According to IMI Daily:

- One-bedroom apartments in Voulgari–Ntepo–Martiou generate around 6%

- While three-bedroom units in Toumpa yield only around 3.2%

This confirms that: The Greek market is increasingly rewarding liquidity, occupancy, and operational efficiency rather than size or premium branding alone.

This marks a major shift in investor behavior.

Previously, many international buyers acquired Greek property primarily for:

- Asset preservation

- Vacation usage

- Or Golden Visa eligibility

Today, however, investors are increasingly asking: “Can this asset generate sustainable income?”

Why smaller apartments are becoming more attractive

A major reason behind this shift is the changing structure of demand in Greece.

Recent data shows:

- Greece recorded approximately 52 million overnight stays in 2025

- The country is now among Europe’s largest short-term accommodation markets

This has created substantial demand for:

- Smaller apartments

- Serviced residences

- Flexible urban accommodation models

Today’s tenant base increasingly includes:

- International tourists

- Remote workers

- Foreign students

- International professionals

- Medium-term residents

Most of these groups prioritize:

- Location

- Transport connectivity

- Flexibility

- And affordability

rather than large apartment sizes.

That is why one-bedroom apartments are currently producing significantly stronger yields across many areas of Athens.

The september 2024 short-term rental restrictions changed the market

One of the most important shifts in Greece’s Golden Visa market came with the September 2024 regulatory changes related to short-term rentals.

Under the new framework: Golden Visa properties can no longer operate under informal Airbnb-style short-term rental structures.

Violations may result in:

- Fines of up to EUR 50,000

- And potentially the revocation of residency permits

This had major implications for the market.

Between 2017 and 2024, areas such as:

- Kolonaki

- Plaka

- Monastiraki

experienced sharp price increases driven by Airbnb demand.

Short-term rentals had significantly boosted effective yields compared to traditional long-term leasing.

But following the regulatory changes: Golden Visa investments are increasingly being evaluated based on long-term operational fundamentals rather than speculative tourism income.

As a result, the market is now shifting:

- Away from speculative Airbnb retail investing

- Toward professionally operated assets supported by genuine residential demand

Why this matters

During the previous cycle, many investors focused on tourist-heavy districts because of:

- Rapid price appreciation

- And exceptionally high Airbnb returns

However, this also caused:

- Overinflated acquisition prices

- Compressed operational margins

- And excessive reliance on short-term tourism

Now that Airbnb-style models are being restricted, the market is returning to more sustainable fundamentals:

- Real residential demand

- Infrastructure

- Connectivity

- And long-term operational viability

This creates a structural advantage for areas:

- With strong local demand

- Reasonable entry prices

- And growing international traffic

And Piraeus is one of the clearest examples.

Piraeus is emerging through real demand

In recent years, Piraeus has benefited from:

- Direct metro connections to Athens

- Rapid growth in cruise tourism

- Expanding logistics infrastructure

- Increasing international visitor flows

More importantly: Property prices in Piraeus still remain significantly lower than many central Athens districts.

This makes the area attractive for investors seeking:

- Earlier-stage pricing

- But rapidly growing operational demand

Unlike districts previously dependent on Airbnb speculation, Piraeus is supported by:

- Real residential demand

- Business travel

- Logistics activity

- Cruise tourism

- And medium-term stays

This creates a far more stable long-term demand structure.

Keranis Residences and the rise of professionally managed real estate

Within this context, projects such as Keranis Residences reflect the market’s new direction quite clearly.

Located along the Athens–Piraeus corridor, the project directly benefits from:

- Metro infrastructure

- International visitor flows

- Urban accommodation demand

- And the growth of professionally managed residential assets

Most importantly: Following the 2024 regulatory changes, the market is increasingly favoring structured operational real estate over informal Airbnb-style investments.

This is why sectors such as:

- Serviced residences

- Urban hospitality

- Professionally managed apartments

are becoming significantly more relevant within Greece’s evolving Golden Visa landscape.

Conclusion

The data highlighted by IMI Daily points to a major transition in Greece’s Golden Visa market.

This is no longer simply about: “Buying property to obtain residency.”

Instead, it is increasingly becoming: A strategy focused on operational real estate, sustainable rental income, and long-term urban growth.

Within this environment:

- Athens continues to lead the market in rental performance

- Smaller apartments are outperforming larger luxury units

- And Piraeus is emerging as one of Greece’s most promising growth corridors due to infrastructure, logistics, and real residential demand

For many international investors, Greece’s Golden Visa market is now evolving: From trend-driven investing to data-driven and operationally focused real estate ownership.